Discover how seller concessions and seller credits work. Learn what they cover, how to negotiate them, and the maximum limits for Conventional, FHA, VA, and USDA loans.

In today’s dynamic real estate market, negotiating a home purchase involves more than just agreeing on a sale price. If you’re a home buyer trying to keep your out-of-pocket expenses low, or a real estate agent looking for creative ways to hold a deal together, seller concessions (often called seller credits) are your best friend.

Whether you’re trying to cover closing costs or buy down an interest rate, understanding how to structure seller credits can make or break a transaction. Let’s dive into exactly what seller concessions are, what they can be used for, and the rules you need to follow based on the loan type.

What Are Seller Concessions?

Seller concessions are closing costs that the seller agrees to pay on behalf of the buyer. Instead of the buyer bringing the full amount of cash to the closing table, the seller essentially redirects a portion of their profit from the sale to cover some of the buyer’s expenses.

For the seller, it might seem counterintuitive to give money back. However, offering a seller credit is often a faster, more effective way to incentivize a buyer than dropping the listing price. For example, a $10,000 seller credit saves the buyer $10,000 in cash on closing day, whereas a $10,000 price reduction might only save the buyer $50 a month on their mortgage.

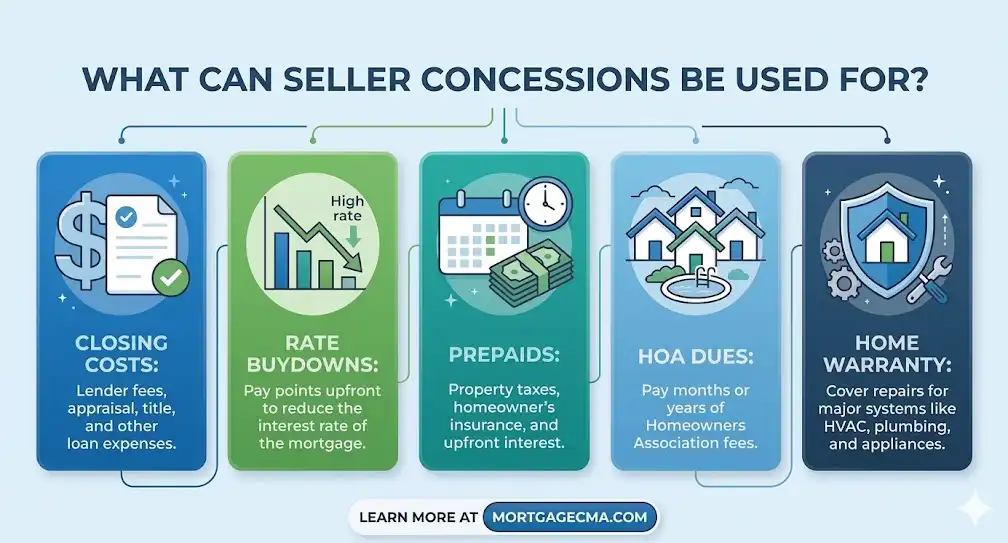

What Can You Use Seller Concessions For?

Seller credits cannot be used for the buyer’s down payment, nor can the buyer walk away from closing with “cash in hand.” However, they can be used for almost all other transaction-related expenses.

Here are the most common ways to use seller concessions:

- Closing Costs: Title insurance fees, appraisal fees, lender origination fees, and escrow fees.

- Rate Discount Points: Paying money upfront to permanently lower the interest rate on the mortgage.

- Temporary Rate Buydowns: Funding a 2-1 or 3-2-1 buydown to lower the buyer’s interest rate for the first few years of the loan.

- Prepaid Items: Funding the buyer’s escrow account for future property taxes and homeowners insurance.

- Upfront Homeowners Association (HOA) Dues: Covering up to one year of HOA dues in advance.

- Home Warranty: Purchasing a 1-year home warranty to protect the buyer against unexpected appliance or system failures.

- Debt Payoff (VA Loans Only): Under specific VA loan guidelines, concessions can even be used to pay off the buyer’s consumer debt to help them qualify.

For Home Buyers: How to Keep Cash in Your Pocket

Buying a home is expensive. Between the down payment, moving trucks, and new furniture, your savings can deplete quickly. Negotiating seller concessions is the smartest way to preserve your liquidity.

Pro Tip: Instead of asking the seller for a $5,000 price reduction, ask for $5,000 in seller credits. If the seller accepts, their bottom line remains the same, but you get to keep $5,000 in your bank account to use for renovations or emergencies.

Talk to your loan officer at Cederholm Mortgage Advisors with Edge Home Finance early in the process. We can help you calculate exactly how much cash you’ll need to close and tell you the maximum seller credit you should ask for based on your specific loan program.

For Real Estate Agents: Using Credits to Save the Deal

As a Realtor, you know that keeping a deal together after a rough inspection can be challenging. Seller concessions are the ultimate problem-solving tool.

- Inspection Negotiations: Instead of forcing the seller to manage contractor repairs before closing (which can delay the timeline), negotiate a seller credit. This allows the buyer to hire their own contractors after closing and keeps the transaction moving.

- Marketing Stagnant Listings: If you have a listing that has been sitting on the market, don’t just drop the price. Advertise “Seller Offering $10,000 Toward Rate Buydown!” This directly targets the buyer’s biggest fear (high interest rates) and creates a more compelling marketing hook.

Maximum Seller Concession Limits by Loan Type

Lenders cap the amount of money a seller can contribute to prevent inflation of property values. It is critical to know these limits before writing the purchase contract.

Here is a quick cheat sheet for maximum seller contributions based on the property and loan type:

(Note: Percentages are based on the sales price or appraised value, whichever is lower).

Ready to Structure Your Winning Offer?

Understanding seller concessions gives you a massive advantage in any real estate market. Whether you want to buy down your interest rate or just bring less cash to closing, our team at Cederholm Mortgage Advisors is here to run the numbers.

Contact Cederholm Mortgage Advisors today to get pre-approved and learn exactly how much you can save with a strategic seller credit!

Helpful External References for Further Reading: